Renting vs. Owning in GTA 5-Year Cost Breakdown (Feb 2025)

Are you currently renting in the Greater Toronto Area (GTA) and wondering if homeownership is the right move for you? Many renters hesitate to take the leap due to high home prices, but does owning actually make better financial sense in the long run? Let’s break it down in simple terms using two scenarios: Buying with 10% down vs. Renting and Buying with 20% down vs. Renting over a 5-year period.

Important: *The figures presented in this analysis are for informational purposes only and are based on estimated market conditions. Actual costs may vary depending on interest rates, property values, taxes, and other factors. Please consult with a qualified real estate or financial professional for personalized advice tailored to your situation.* Please also checkout my post about the Pros and Cons of Buying Vs Renting.

The True Cost of Renting Over 5 Years

If you’re renting a one-bedroom apartment in the GTA, you’re likely paying around $2,424 per month (based on Q4 2024 TRREB Rental Market Report). But rent typically increases each year due to inflation,for rental units with no rent control, increase maybe greater than the guideline posted, visit Ontario.ca for more info. Assuming a 2% annual rent increase, here’s what happens over 5 years:

- Total rent paid over 5 years: ~$151,375

- Equity built: $0 (since you don’t own the property)

That’s over $150,000 spent on housing with no return on investment. Now, let’s see what happens if you buy instead.

Use the calculators on Realtor.ca, a trusted tool to help estimate your payments, affordability and plan your home purchase.

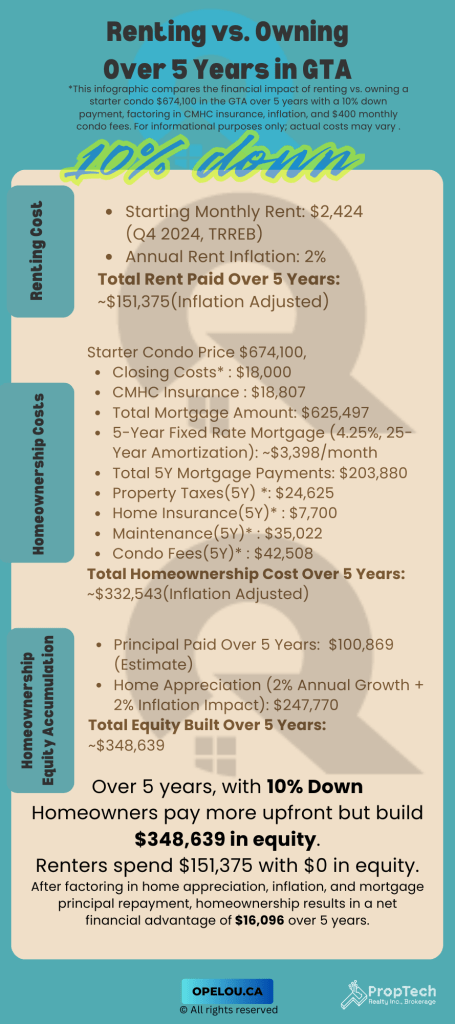

Buying a Condo in GTA with 10% Down Payment

For those looking to buy with a 10% down payment as First Home Buyers, let’s assume the average starter condo price is $674,100(Bench Mark Price for Toronto Apartment). After adding CMHC insurance (required for down payments under 20%), the total mortgage amount is around $625,497. Click here to use calculators on Realtor.ca

Breakdown of Upfront Costs:

- Down payment (10%): ~$67,410

- CMHC insurance: ~$18,807

- Closing costs (legal fees, land transfer tax, adjustments, etc.): ~$18,000

- Total upfront cost: ~$104,217

Breakdown of Expenses Over 5 Years:

- Mortgage payments (5 years at 4.25%): ~$203,880

- Property taxes (estimated 0.7% per year, inflation adjusted): ~$24,625

- Home insurance ($1,500/year, inflation adjusted): ~$7,700

- Maintenance (1% of home value per year, inflation adjusted): ~$35,022

- Condo fees ($400/month, inflation adjusted): ~$42,508

- Total cost of owning over 5 years: ~$332,543

Financial Impact:

- Equity built (mortgage paydown + 2% annual appreciation): ~$348,639

- Net financial position after 5 years: + ~$16,096

Key takeaway: Even with a smaller down payment and CMHC insurance, homeowners in this scenario end up ahead by over $16,000 due to equity growth.

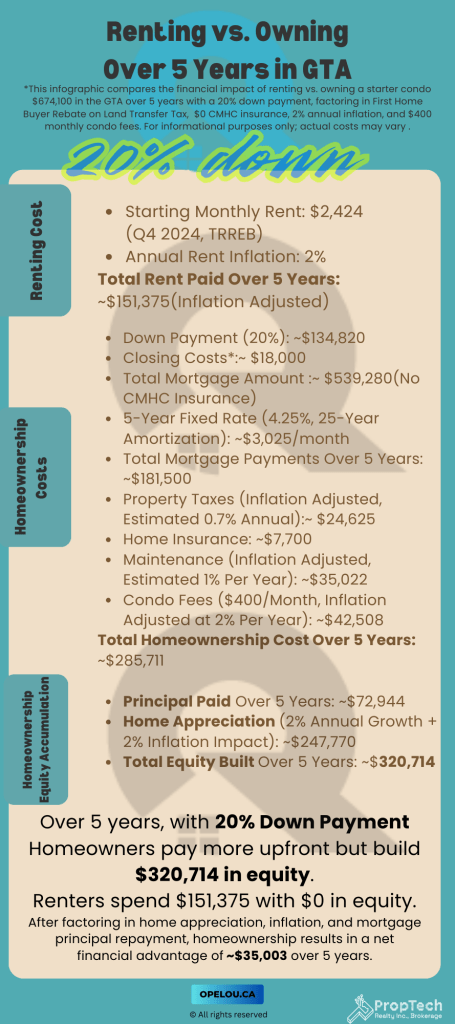

Buying a Condo in GTA with 20% Down Payment as First Home Buyers

Now, let’s see how things change if you put 20% down ($134,820) to avoid CMHC insurance.

Breakdown of Upfront Costs:

- Down payment (20%): ~$134,820

- Closing costs (legal fees, land transfer tax, adjustments, etc.): ~$18,000(Possibly lower if buying outside of City of Toronto)

- Total upfront cost: ~$152,820

Breakdown of Expenses Over 5 Years:

- Mortgage payments (5 years at 4.25%): ~$181,500

- Property taxes (estimated 0.7% per year, inflation adjusted): ~$24,625

- Home insurance ($1,500/year, inflation adjusted): ~$7,700

- Maintenance (1% of home value per year, inflation adjusted): ~$35,022

- Condo fees ($400/month, inflation adjusted): ~$42,508

- Total cost of owning over 5 years: ~$285,711

Financial Impact:

- Equity built (mortgage paydown + 2% annual appreciation): ~$320,714

- Net financial position after 5 years: + ~$35,003

Key takeaway: A larger down payment reduces mortgage costs and helps you build equity faster, leaving you over $35,000 ahead compared to just renting.

So, Is Buying or Renting the Better Option?

If you continue renting, you’ll spend over $150,000 on rent in the next 5 years without building any wealth.

If you buy, even with a 10% down payment, you’ll build equity and potentially come out ahead financially. With 20% down, the financial benefits are even greater, giving you more stability and long-term savings.

Final Thoughts:

🏠 Buying with 10% down: More upfront costs but builds equity, leaving you ahead by ~$16,096. 🏡 Buying with 20% down: Lower total costs, faster equity growth, and a net gain of ~$35,003. 🚪 Renting: ~$151,375 spent with $0 equity built.

While homeownership requires financial planning, it’s clear that over time, buying in the GTA allows you to turn housing costs into an investment rather than an expense.

Thinking about making the switch from renting to owning? Let’s discuss your options!

Have feedback or questions? Please drop an email to Opel Ou, Real Estate Broker: opel@opelou.com

#RentVsOwn #GTARealEstate #Homeownership #FirstTimeBuyer #TorontoHomes #RealEstateInvesting #MortgageTips #FinancialFreedom #BuyOrRent #WealthBuilding #RealEstateMarket #TorontoCondos #HomeBuyingTips #PropertyInvestment #HousingMarket #RentingVsOwning #GTAHousing #MoneyMatters #SmartInvesting #MortgageCalculator #RealEstateBroker #Realtor #OpelOu